Retirement Planning and Investing Research

Below you’ll find a listing of all of the research I’ve read about retirement planning and investing (well, at least the research I’ve uploaded. Much more to come). The research includes academic articles, white papers, blog posts, podcasts, videos, and even Twitter threads. I include anything that I find interesting, useful, or important. You can search through my research archives in the Topics dropdown to the right.

-

Estimating the True Cost of Retirement

Publication Year: 2013

Spending in retirement does not keep pace with inflation, instead declining on a real basis through mid-retirement and then increasing toward end of life due to healthcare expenses.

-

Kentucky Windage for Asset Allocation

Publication Year: 2022

The paper provides simple adjustments one can make to their asset allocation to adjust for the embedded tax liability of a pre-tax IRA.

-

Spending Trajectories After Age 65

Publication Year: 2022

Retirees spend less, on an after-inflation basis, as they age, regardless of income.

-

Asset Allocation for a Lifetime

Publication Year: 1996

This paper follows his famous 1994 paper on the 4% rule and addresses six questions: (1) should retirees reduce their stock allocation each year, (2) what should their asset allocation be at retirement, (3) how the 4% rule works in taxable accounts, (4) taking withdraws in excess of 4%, (5) how early retirement affects the 4% rule, and (6) asset allocation before retirement.

-

J.P. Morgan 2024 Guide to Retirement

Publication Year: 2024

Offers data on retirement topics, such as longevity, savings requirements and Social Security claiming strategies.

-

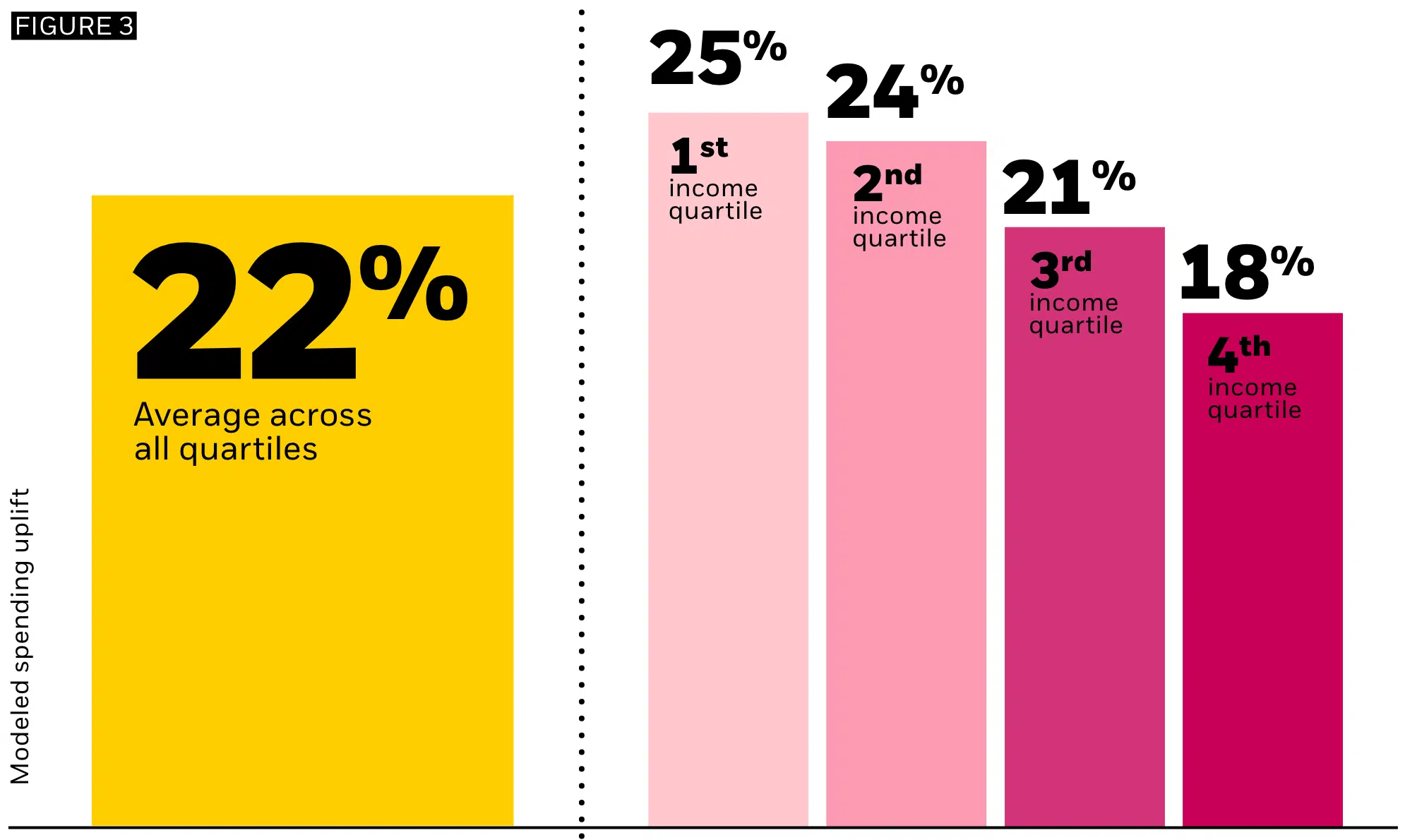

When Nest Eggs Need a Safety Net

Publication Year: 2023

Retirees of all income levels can increase their retirement spending and protect against longevity risk by buying an income annuity with 30% of their retirement savings

Blackrock’s study noted two seemingly contradictory findings. First, according to a 2023 Blackrock study (BlackRock, Read on Retirement™, 2023.), only 21% of workers believe they will have enough money to last through retirement. Second, a 2018 Blockrock study (BlackRock, EBRI, “To Spend or Not to Spend,” 2023 (updated from 2018)) found that most retirees had 80% of their pre-retirement savings after two decades of retirement. These results were found across all income levels, leading Blockrock to conclude that it’s a behavioral issue, namely, that retirees don’t like watching a “leaky bank account.”

To address this issue, Blackrock ran simulations in which the retiree used 30% of their savings to buy an income annuity, investing the rest in stocks and bonds in a 50/50 portfolio. The results, according to Blackrock, is that the addition of the annuity increased spending across all income levels by an average of 22%.

-

Total-Return Investing: A Smart Response To Shrinking Yields

Publication Year: 2021

Total-return investing generates more retirement spending than income-focused investing, even in a low-yield environment.

-

What If You Invested at the Peak Right Before the 2008 Crisis

Publication Year: 2024

If you had invested at the market peak just before the 2008 financial crash, you still would have earned a 9.5% annual return through March 2024, suggesting that we shouldn’t obsess over valuations as long-term, buy-and-hold investors.

-

The State of Retirement Income 2021

Publication Year: 2021

Using forward-looking estimates of market returns and inflation, the report concludes that 3.3%, not 4%, is the new safe withdrawal rate.

-

Reality Retirement Planning: A New Paradigm for an Old Science

Publication Year: 2005

Retirement withdraw plans should reflect a real (after-inflation) decline in spending, which enables an early retirement and spending more during one’s “go-go” years of retirement.