Empower Review and User’s Guide (Updated July 2026)

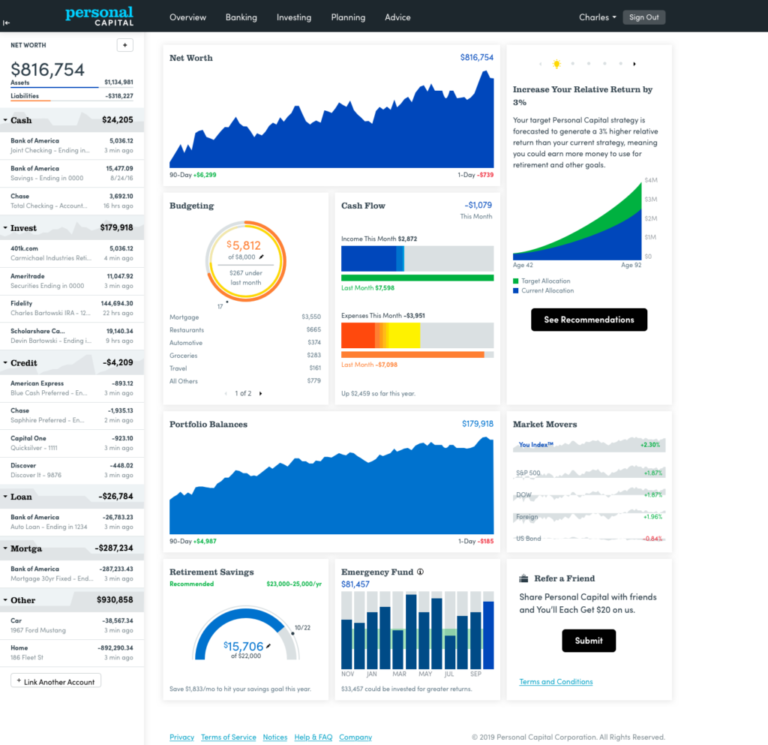

Empower is a financial tool that enables you to manage 100% of your finances from a single dashboard. Previously called Personal Capital, I’ve used the app for years. In this Empower review and user’s guide, I’ll walk through all of its features and how to leverage them to help you make the most of your…