7 Simple Calculations that Show the Awesome Power of Compound Interest

We earn a commission from the offers on this page, which influences which offers are displayed and how and where the offers appear. Learn more here.

Albert Einstein purportedly said “compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.” The question is how do we understand it? We can start by running 7 calculations that demonstrate the power compounding.

What is Compound Interest?

Compounding occurs when investments grow in value based on their original investment and any interest, dividends or other earnings they’ve generated. For example, savings accounts typically pay interest on balances each month. If the starting balance is $1,000 and the first interest payment is $10, the next month’s interest payment will be made on the new balance of $1,010. This repeats indefinitely. Stocks and bonds take advantage of this favorable math, too.

Compounding starts off slow. Even after a few years of saving and investing, most of the balance comes from the money you’ve saved, not compounding. Give it some time, however, and compounding will generate far more in wealth than the actual dollars saved. Here are 7 calculations that demonstrate this power.

7 Compound Interest Calculations

For these calculations we’ll use a compound interest tool I created in Excel that you are welcome to use. For these calculations we’ll assume the following:

- We earn $50,000 a year for our entire working life. A generous salary for a 20-year-old but it evens out since their salary is remaining constant for decades.

- Our savings rate will also stay constant at 5 percent. That works out to $208.33 in monthly investable savings.

- We save for 45 years, a typical working career.

Now if we saved this money but never invested it, we’d end up with a total retirement fund of $112,500. That’s only $4,500 in yearly retirement income assuming a 4 percent withdrawal rate. Not exactly living high on the hog. The following 7 calculations will make this story more encouraging.

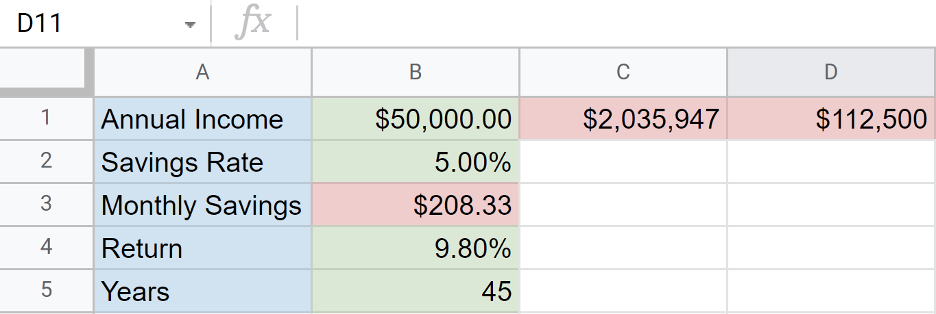

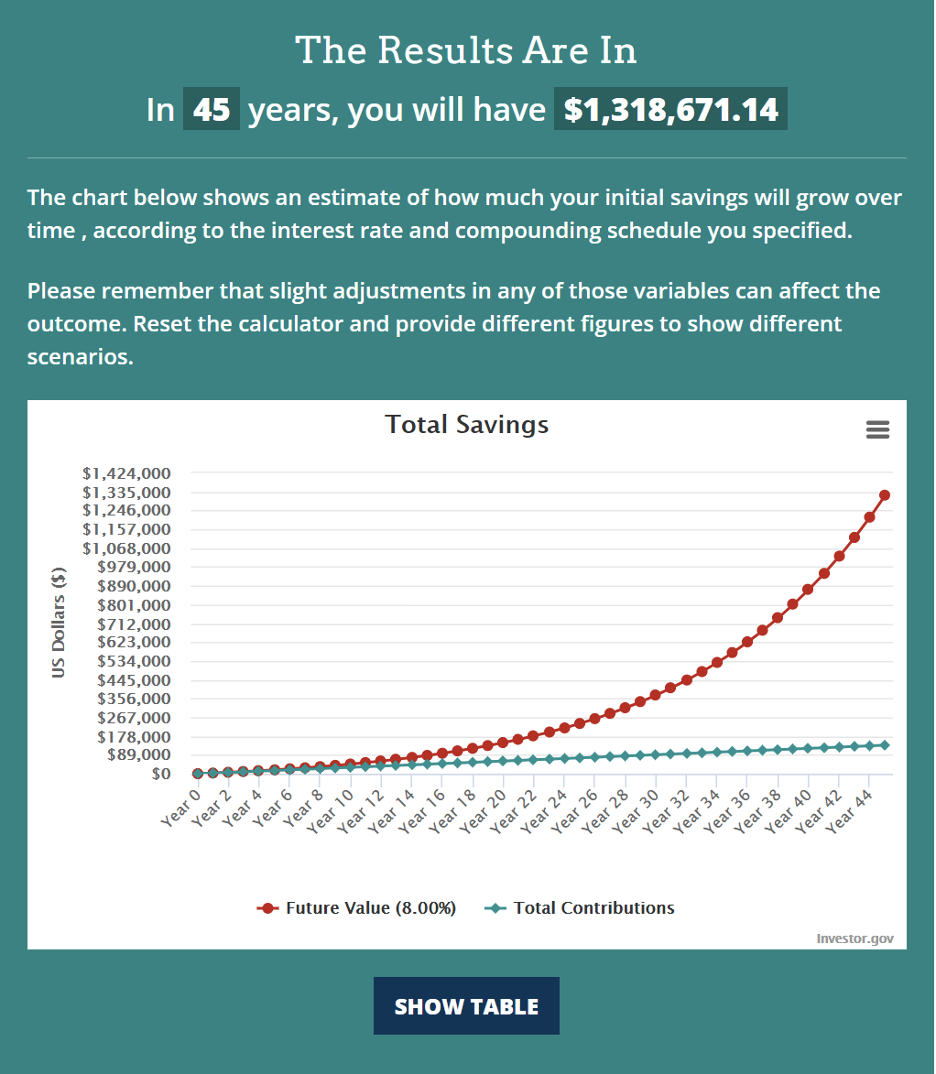

Calculation One: We earn a 9.8% return

The only variable we’re going to change for the first calculation is the rate of return on our savings. Instead of zero percent appreciation, we’re going to assume a 9.8% compounding return on their money. Why 9.8 percent? Vanguard studied market data from 1926-2020 and found that a portfolio of 80 percent stocks and 20 percent bonds returned an annualized 9.8 percent. The best way to achieve the kinds of returns Vanguard studied is to invest in low-cost index funds. A 3-fund portfolio is one approach.

Hitting enter on the tool shows that investing the same savings from the control example yields an end balance of $2,035,947. A healthy return considering monthly contributions can be completely automated through brokerages like M1 Finance. The real work is in diligently saving and patiently waiting for compound interest to do the rest.

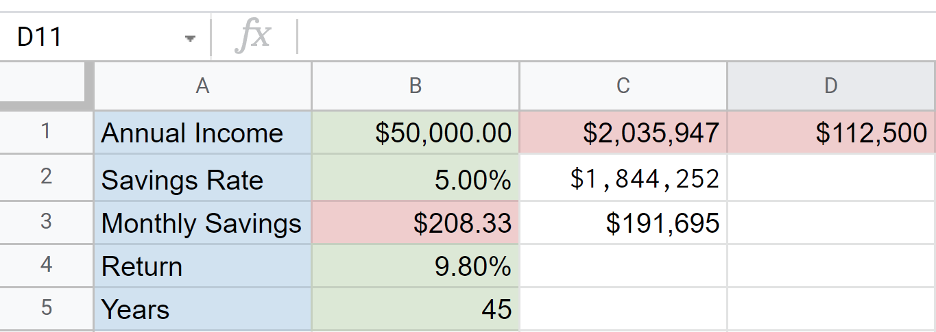

Calculation Two: We save for 44 years instead of 45

What happens if we change the time horizon for retirement? Changing the contribution timeline from 45 years to 44 years might have a larger impact than you might think.

Instead of an ending balance of $2,035,947 we get $1,844,252. That’s a difference of $191,695. So shaving even one year off of an investing time horizon can cut out exponential gains. How should this realization fit into financial planning?

Some personalities in the investing space advocate paying off all debt before investing, even considering the boost tax-deferred accounts and company matches give. The math behind compound interest makes that advice seem rather tenuous.

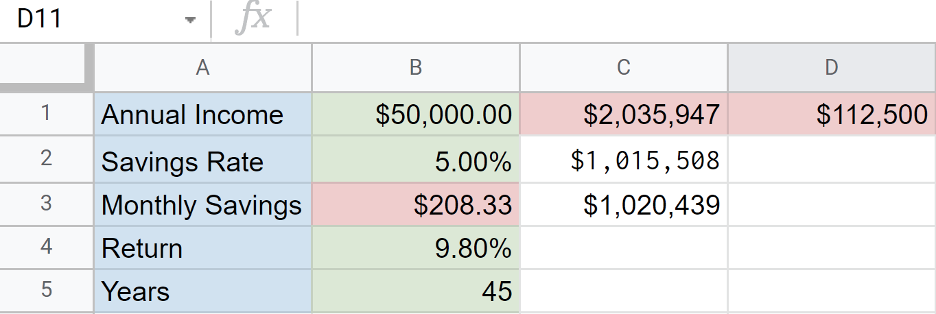

Calculation Three: Invest for 38 years instead of 45

Let’s assume a scenario in which our worker pours all their investable savings into paying down low-interest student loan debt before investing. If it takes them 7 years to pay off their school loans, it cuts their investing timeline down to 38 years instead of 45 years.

The loss of those seven years cost them more than $1 million in lost wealth.

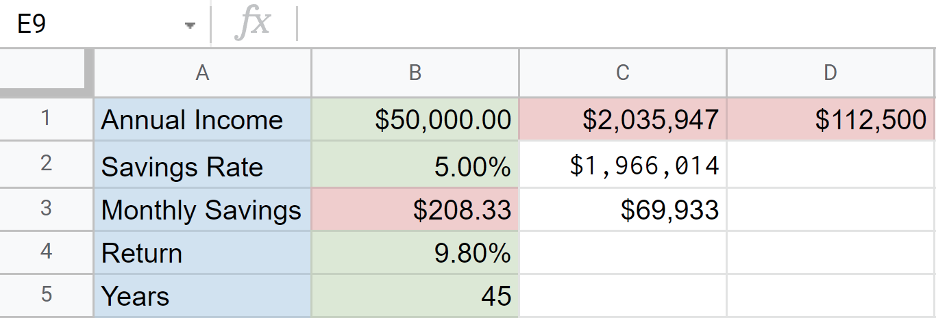

Calculation Four: We earn 9.7% instead of 9.8%

If time horizon is so important, how important are fees? If we reduce our expected returns by subtracting just 10 basis points (0.10%) in fees from the yearly return expectation, we can see just how important fees are.

Almost $70,000 less for retirement. There’s no way of telling what the market will return over the next 45 years. On the other hand, we can choose exactly what amount of fees we pay. And that brings us to the next calculation.

Calculation Five: We earn 8.8% instead of 9.8%

One-tenth of one percent in fees docked us $70,000. Now let’s assume our worker pays the market rate for a fiduciary. Fiduciaries typically charge one percent of a portfolio’s value for their services. That brings our expected return down from 9.8 percent to 8.8 percent.

It turns out that one percent in fees equates to almost $600,000 in lost retirement assets. That’s a big price to pay for peace of mind and a strong case for DIY investing.

You can use the free tools offered by Personal Capital to determine what fees you are paying on your investments and how those fees will affect your wealth over time.

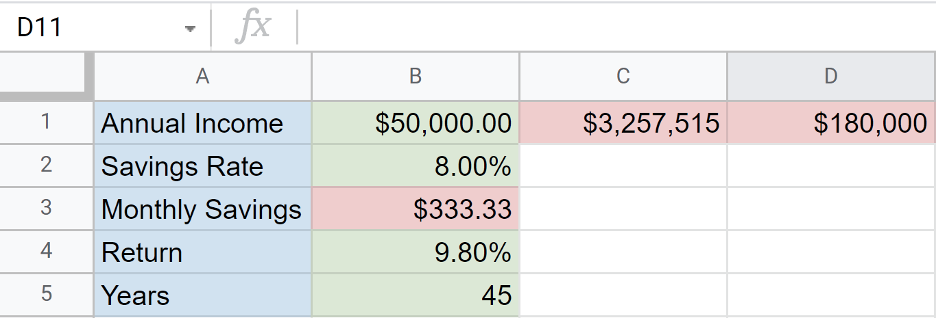

Calculation Six: We get a 3% company match

We’ve explored the role expected returns have on compounding. Savings rate plays a large role as well. Let’s assume that an employer agrees to match 3%of our worker’s annual salary. That bumps up the savings rate from 5%to 8%. The monthly contribution jumps from $208.33 to $333.33. $125 more going into the market every month.

Best of all, that extra $125 is essentially free money, with no additional sacrifice needed. Saving that extra 3%could require noticeable belt-tightening without the aid of an employer match.

The employer match changes a $2,035,947 retirement nest egg into $3,257,515. That’s an increase of $1,221,568 and more math to support taking advantage of employer contribution matches even if low-interest debt could be paid off instead.

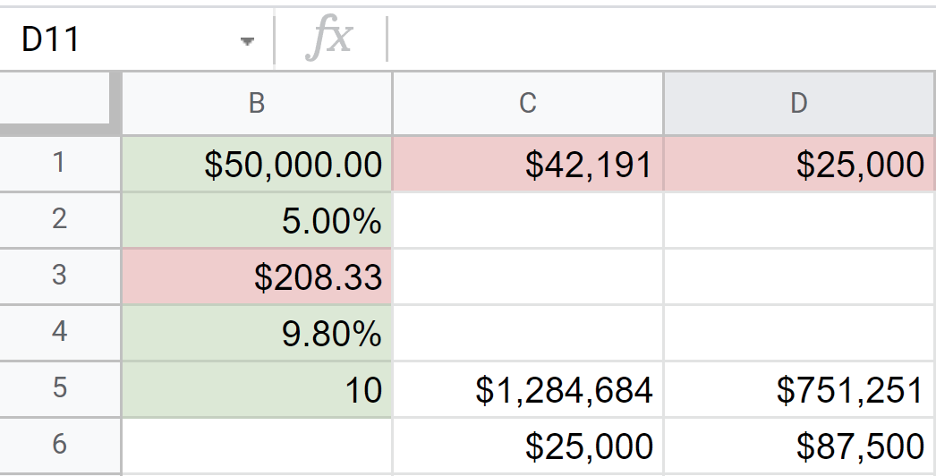

Calculation Seven: Saving early versus saving late

Let’s put it all together and find out where exactly the awesome power of compounding interest is. Cutting the investing window down to 10 years yields a $42,191 portfolio. That’s only a $17,191 return on $25,000 invested. Investor.gov provides a calculator that shows the tight grouping of invested money and total portfolio value in the early decades of investing.

Let’s assume that after reaching 10 years of contributions, our worker stops adding to their portfolio. The $42,191 continues to grow for another 35 years without being touched. Compounding alone carries the portfolio to a value of $1,284,684, all from just $25,000 in invested savings.

Contrasting that happy scenario with a different approach should be telling. In our second example, let’s say our worker waited 10 years to start investing. That cuts their investing window down to 35 years instead of 45 years. But we’ll assume they save and invest for the remaining 35 years.

Their contributions over those years add up to $87,500. That’s $62,500 more savings invested than our first example. However, their portfolio only reaches a value of $751,263. Over $500,000 less than our start early, set-it-and-forget friend.

Final Thoughts

We managed to avoid any theoretical physics thankfully. All the compound interest insights we needed were from some basic arithmetic. Compound interest is a powerful force so it’s best to work with it rather than without it. To best capture its potential, investors should take care to make a few key choices.

For starters, invest. Money can’t compound if nothing is being reinvested over time. Second, start early. Gains grow exponentially. The latter years of investment gains will far exceed whatever principle was contributed in early years.

Third, consider contributing to retirement even while carrying low-interest debt. Being debt-free might seem psychologically appealing, but the math behind compounding begs that we invest early and often. Fourth, fees can stunt returns. Be wary of investing in funds or with advisors that charge fees well beyond what you would pay by investing in low-cost index funds.

Fifth, take advantage of employer matching programs. More money being contributed is more money to be compounded. Finally, money investing in your twenties is markedly more valuable than money investing in later decades. But, as they say, the best time to invest was twenty years ago, the second-best time is now.